On August 5, 2026, The Chemours Company FC, LLC (“Petitioner” or “Chemours”) filed a petition requesting the imposition of antidumping and countervailing duties on imports of perfluoroalkoxy alkane (“PFA”) from…

On August 3, 2026, the state attorney generals of twenty-five states (25) co-led by State of Oregon, Arizona and California filed a complaint in the Court of International Trade (CIT)…

On July 31, 2026, President Trump issued proclamation “To Facilitate Positive Adjustment to Competition From Imports of Quartz Surface Products,” introducing a tariff-rate quota (“TRQ”) that will go…

On July 28, 2026, the U.S. Department of Commerce (Commerce) published a federal notice stating that U.S. manufacturers of engines for cars and medium- and heavy-duty trucks (MHDVs) can now…

On July 29, the Federal Communications Commission (FCC) updated its Covered List to add two new categories of foreign-produced equipment: advanced robotic devices and power inverters. The move follows determinations…

On July 29, 2026, the Hydraulic Cylinders Fair Trade Coalition and its individual members, Aggressive Hydraulics, Inc., Hol-Mac Corporation, Ligon Hydraulics, Prince Manufacturing Corporation, PTC Alliance LLC, Rosenboom Machine &…

United States and Jordan Sign Reciprocal Trade Agreement

On July 21, 2026, the United States and Jordan signed a reciprocal trade agreement under which Jordan will receive a preferential 10%…

After the May 2026 Supreme Court ruling in Montgomery v. Caribe Transport II, LLC, one critical question remained unanswered: whether the safety exception extends to cargo theft and property…

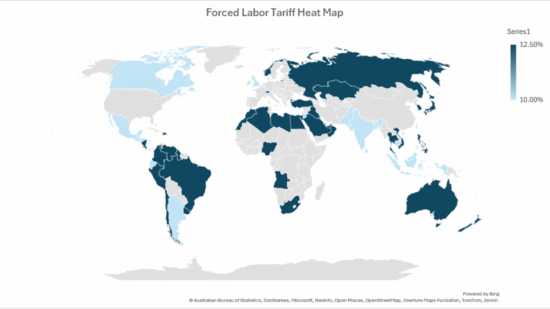

The Office of the United States Trade Representative (USTR) has announced the imposition of new Section 301 tariffs under the Trade Act of 1974. Following investigations into global forced labor policies…

The U.S. Department of Justice (DOJ) and the Department of Homeland Security (DHS) have sent a clear message that the era of treating customs fraud as a manageable cost of…